This article is not financial advice, and it’s for informational purposes only. It’s not a solicitation or recommendation. Crypto is volatile, changes rapidly, and I’m just some guy on the Internet writing about it. Engage at your own risk.

Say you’ve bought some Bitcoin and seen it shoot up in value over the last year or two.

You keep hearing that crypto will “change the world” or “be the new Internet,” but as far as you can tell it’s mostly just speculative assets that continue to appreciate… for some reason.

You might want to explore more, but the world of crypto is painfully opaque. Everyone talking about it on Twitter is using weird new acronyms, and half of them have a cartoon character or pixelated punk as their avatar. It’s interesting but geeky and confusing, so you’re not sure where to start or even who to listen to.

I had been sitting on the sidelines, passively buying Bitcoin for years, and in the last few months I decided to go deeper. I wanted to know what was really special about this technology. Why should I care? And why was it appreciating so much in value?

In this series of posts, I’m going to share what I’ve been learning, and how you might dive deeper into the world of crypto, both from the financial investing side and the pure curiosity side.

I’m assuming that if you’re here, you’ve already bought a bit of Bitcoin and maybe Ethereum, but it’s sitting in Coinbase while you wait for it to go up. That’s a great place to start. And if you’re not there already, I’d open up an account, set up some weekly or monthly buys, and let your investment drive your curiosity.

But once that’s done, what’s next? Coinbase made it so easy to get into crypto, but the next steps are unclear.

In this post, I’ll go over what I think a good next step is: Using crypto to create a high-yield savings account.

What is a Savings Account

A savings account is like a magic box that grows your fiat money. You park some cash in it, and in it pays you some interest in exchange. Or it used to anyway.

For a brief period a few years ago online cash savings accounts like Wealthfront were offering around 3% interest. This isn’t a ton, but it’s not bad for what is almost as close to a “zero risk” investment as you’re going to get.

But with cuts to the federal funds rate, those savings rates have dwindled. The current APY is only 0.10%, which means that at 2% inflation, you’re losing about 2% of your cash’s value by having it in a savings account each year. Boo.

To understand why things are this way, you have to understand how banks make money. When you put your money into a savings account, banks lend it out to borrowers for things like mortgages. They make money on the difference between what they charge borrowers for loans, and what they pay you for putting money in your savings account. This means that if mortgage rates are low, the interest banks can afford to give you on your savings account is near zero.

So while it’s great that we can currently get mortgages at below 3% interest, it’s terrible for our savings accounts. With debt being that cheap, there’s no room left for banks to pay you interest on your savings, which has made savings accounts basically worthless.

But traditional banks aren’t the only entities that will pay us interest for storing our money with them. There’s an emerging new world of “decentralized finance” (also called “DeFi”) we can tap into.

What is Decentralized Finance

When you store your money with Chase, Chase bank decides what happens to it. They set the interest rates, they administer the loans, get drunk on champagne, overwork their first years, and fly around on private jets.

Banks are centralized. There’s a board of directors, CEO, and employees who are deciding what happens with your money. Including whether or not you can even access it!

Historically this was the only option. You couldn’t just throw your money in a pile in a warehouse downtown and trust everyone else to only take out their share of it. We needed a “trusted third party” to handle our money for us.

Now that’s changing. With code and crypto technology, we can build a whole new suite of financial institutions that run on code instead of 24-year-olds. Instead of Topher from Dartmouth deciding whether or not you get a loan, software can automatically decide it for you.

The efficiency and cost savings of these applications is mind-blowing. Coinbase IPO’d two weeks ago, and they’ve built an incredible crypto exchange that employs 1,200 people. But there’s another crypto exchange you might not know about: Uniswap, which does as much trading volume as Coinbase but only has 12 employees. Same throughput, 1/100th the employees. How? It’s a decentralized financial application.

To understand how these DeFi applications work, let’s look at one of my favorite projects in the space that’s a little easier to understand: Compound. Compound is “an algorithmic, autonomous interest rate protocol.” For comparison, you might call Chase a “centralized, managed interest rate protocol.” Compound does the same lending processes we outlined earlier: paying interest on stored funds, and collecting interest on loaned funds, but they do it all with code instead of bankers. And they currently have about $15,500,000,000 in assets under management, about the same as Wealthfront.

You can put money into Compound, and the protocol will pay you interest for storing your money there. And you can borrow money from it, which you’ll have to pay interest on. And just like with a normal bank, Compound makes money by charging more interest to borrowers than it pays to lenders.

Here’s the big difference though. Compound is a decentralized autonomous application, so instead of the earnings being collected by the bank’s executives, the earnings are distributed to the people using the bank. This happens through a cryptocurrency that Compound continually mints and issues to their users called COMP, and which you can also buy and sell on Coinbase and other exchanges. As money is stored on Compound, new COMP tokens are created and paid out to users both on the Lend and Borrow side.

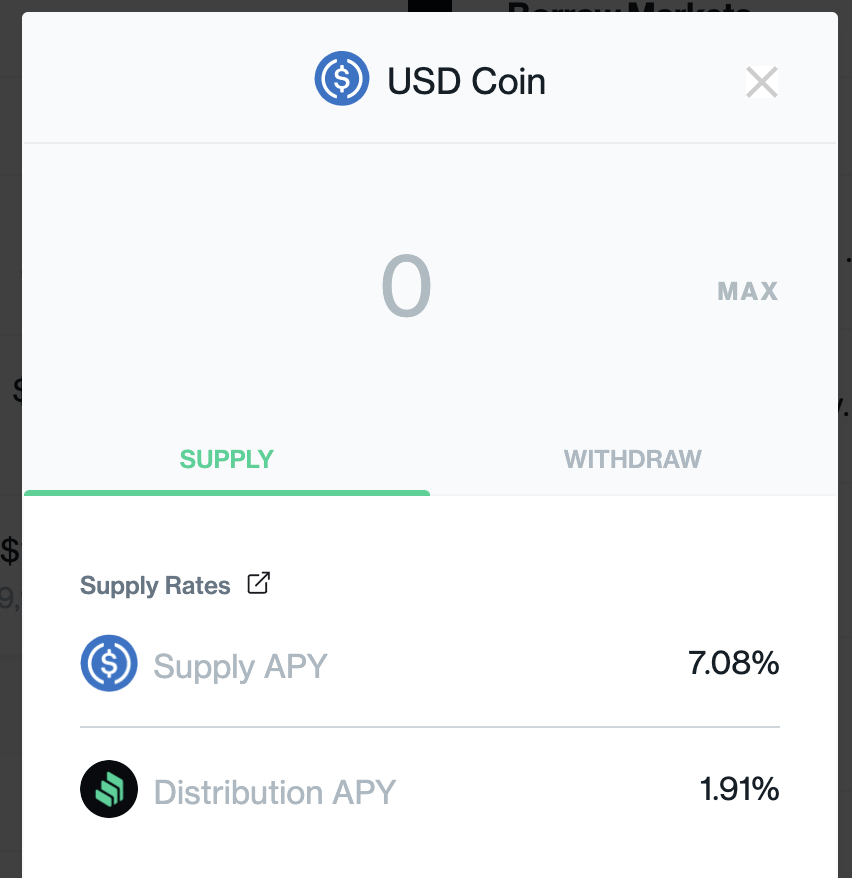

So right now if you lend money to Compound, you currently earn 7.08% interest in dollars, but you also earn an extra 1.91% interest in COMP tokens. You’re earning interest on your dollars in dollars, but you’re also earning a bit of interest in the platform. Think of it like if you automatically earned JP Morgan Chase stock based on how much money you stored there.

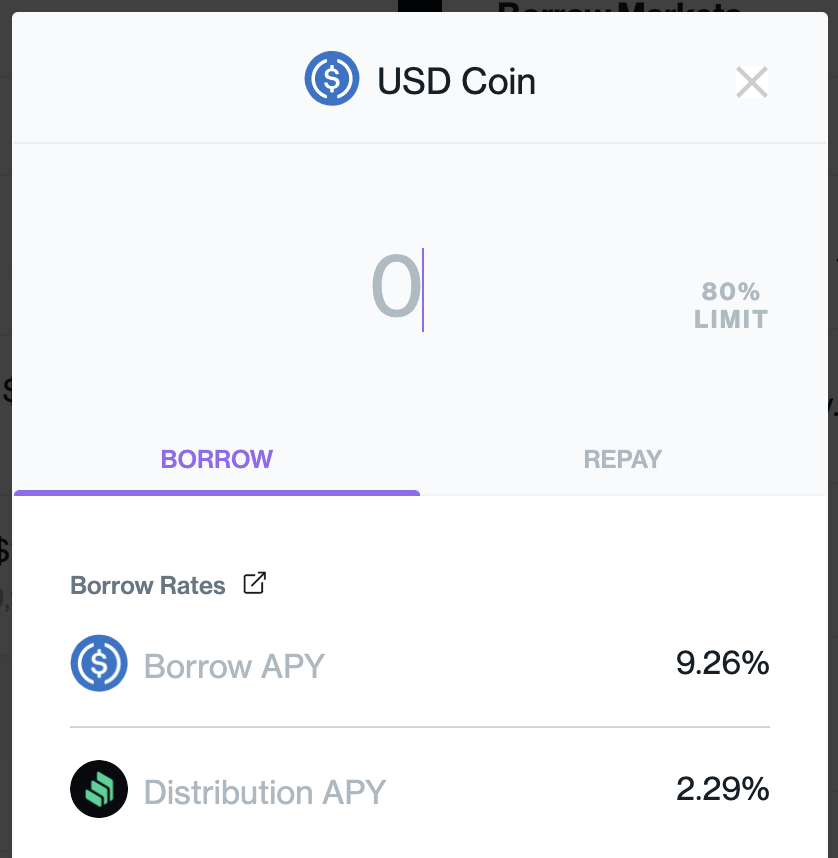

They can offer that interest rate to lenders because if you go to Compound as a borrower, you’re going to pay quite a bit more. The typical spread between the rate they pay to lenders and the rate you pay to borrow is 2-3% depending on the day and which currency you’re looking at:

Wait, What?

At first glance this seems suspiciously good. There’s a place where you can just put money in and earn 3 to 8% auto-compounding interest on it? And you can just take out a loan without going through underwriting? What’s going on here?

Part of the discrepancy in potential gains between using something like Compound and using a traditional financial institution is the efficiency of having the whole system run autonomously. Wealthfront, which has about the same amount of assets under management, employs around 250 people. It’s hard to figure out how many people work at Compound but it’s somewhere between 11 and 50.

The system works because when you deposit money on Compound and stake it as collateral, Compound can automatically liquidate your collateral if you get overleveraged. You can read more about the details here if you’re curious, but suffice it to say that the code underlying Compound prevents the system from blowing up the way banks did in 2008. At least as far as we know, and based on the auditing by other companies which you can read about here.

But who’s using Compound to borrow money? And why would someone borrow money from Compound when they can go to a traditional bank? Because with Compound, there’s no approval process. As long as you’ve staked some amount of your crypto on Compound, you can borrow against that crypto, usually around 75% of the value of what you’ve staked.

So if you join Compound and put up $10,000 of collateral, you can instantly borrow $7,500 of USDC or another cryptocurrency. No questions asked. And you can repay it on whatever timeline you want, but you’ll keep accruing interest until you do.

And while it might be a high-interest rate compared to what you can get for a mortgage or car loan, it’s lower and significantly more convenient than what you’d have to pay for a hard money or P2P loan.

So if you wanted to take some of your cash savings in a traditional bank and park them in a DeFi protocol like Compound to earn better interest rates, what’s the best way to do that?

Setting Up Your DeFi “Savings Account”

Before we dive in let’s talk about risk. DeFi is very early, and there are still some unknowns. Compound has been in operation since 2018 and has gone through a number of security audits, but there are definitely some unknown unknowns. Just like a regular bank, something could go wrong and it could blow up.

The difference though is that at a regular bank, you have FDIC insurance for up to $250,000 of your savings. Compound can’t offer that. If it blows up, you could lose everything you put into it. But you can be smart with managing your risk. Using a variety of platforms (like Aave, BlockFi, etc.) can help spread out your risk so that you aren’t trusting a single platform. And you can buy insurance (also decentralized!) against the platform blowing up.

So is it really a “Savings Account” in the sense you’re familiar with? Not exactly. But it’s about as close as we have right now in the world of DeFi, and I think of my money in Compound the same way I think of my Wealthfront Cash account. You have to decide for yourself how much you trust these platforms vs. older institutions.

I personally have half my cash savings split between DeFi and TradFi. That’s not a recommendation, that’s just so you know how much skin in the game I have.

If you decide it’s something you want to try, start by taking whatever amount you want to save and use it to buy USDC on Coinbase. USDC is a stablecoin: a cryptocurrency that’s pegged to the US Dollar, so it will always be $1. You can read more about how that works here if you’re curious. Stablecoins like USDC are great because they let you move some of your money into the crypto economy, without being exposed to the wild price fluctuations you might see with Bitcoin and other assets.

I should mention one other thing though before we continue. As of this writing, doing anything on Ethereum (like setting up this Compound account) is pretty expensive since there’s a transaction fee for each action. Unless you plan on moving at least a few thousand dollars and letting it sit for a year, it might not make sense to do this until transaction costs on Ethereum come down.

Assuming you’re willing to move enough for it to make sense though, here’s what you do next.

To transfer your USDC into Compound, you’ll need a browser wallet like MetaMask. Follow the instructions on their site, and you should be good to go in a few minutes. Just make sure you write down your recovery phrase somewhere safe!

Once your MetaMask is set up, you’ll be able to transfer your USDC from Coinbase to your MetaMask wallet. Then from there, all you need to do is go to app.compound.finance, click on USDC, and deposit your funds!

Once your funds are deposited, you’ll start earning interest in both USDC and COMP. The USDC is automatically added to your USDC contribution, which means your interest is being constantly compounded. The COMP you’re earning gets tracked as a credit to your account, and when it gets to a big enough amount to justify paying the transaction fee to claim it, you’ll be able to collect the COMP you earned and either sell it or lend it to Compound to earn more interest.

And that’s it! Any time you want to deposit more you can buy more USDC and transfer it over. Then if you want to take things to the next level, you can consider letting some other DeFi software optimize your asset allocation for you.

Find Out What

Comes Next in Tech.

Start your free trial.

New ideas to help you build the future—in your inbox, every day. Trusted by over 75,000 readers.

SubscribeAlready have an account? Sign in

What's included?

-

Unlimited access to our daily essays by Dan Shipper, Evan Armstrong, and a roster of the best tech writers on the internet

Unlimited access to our daily essays by Dan Shipper, Evan Armstrong, and a roster of the best tech writers on the internet

-

Full access to an archive of hundreds of in-depth articles

-

-

Priority access and subscriber-only discounts to courses, events, and more

-

Ad-free experience

-

Access to our Discord community

Dan Shipper

Dan Shipper

Evan Armstrong

Evan Armstrong

Comments

Don't have an account? Sign up!

Nat- thanks for the beginner’s guide. I think it would be worth mentioning taxes. Any crypto to crypto conversion is a taxable event and it seems really difficult (at present) to clearly follow tax lots.

Great article! Any idea on how it works in terms of filing taxes. Do they provide a tax statement end of year like Banks do?

Love the article!

Any thoughts on anchor protocol?